In the realm of financial trading, a directed order is a specific instruction a trader gives to a broker to send a trade order to a particular market maker or specialists for execution. Traders may direct orders if they believe a particular venue can offer a more favorable outcome, which might be in the form of a better price, faster execution, or the likelihood of trade completion. These instructions surpass the automated order routing systems that typically handle trade orders via algorithms that seek the best available terms.

Such orders offer an additional layer of control for investors who have preferences regarding the execution of their trades. By directing orders, they aim to influence the path and eventual execution point of their trade, potentially benefiting from the nuances of different execution methods. Directed orders are also significant in broker-dealer dynamics as they allow for the negotiation of terms that may not be otherwise available through non-directed pathways.

Key Takeaways

- Directed orders allow traders to specify the execution venue for their trades.

- They provide traders with control over the trade execution process.

- The existence of directed orders underscores the complexity and customization available in modern financial markets.

Understanding Directed Orders

In financial markets, directed orders play a crucial role in the execution process, affecting the order flow and ultimately impacting both liquidity and execution prices. We’ll explore the basics, execution, and the benefits and risks associated with these types of orders.

Definition and Basics of Directed Orders

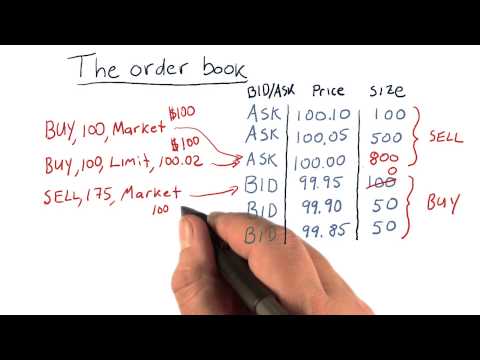

A directed order refers to an instruction that traders or investors give to a broker, signaling that a trade should be routed to a particular market maker or exchange. This kind of order is a binary relation in the order flow, which essentially means it is a set of preferences that prioritize where the order should be executed. Normally, when an order is placed without a specific direction, a broker-dealer may choose where to fill the order, often seeking the best execution based on factors such as price, speed, and likelihood of execution.

In the realm of mathematics, directed orders have a more formal definition as a type of partially ordered set. In this context, partial order is a binary relation that is transitive, antisymmetric, and reflexive. However, within financial markets, the term is used more casually to refer to any order where the trader or investor gives specific instructions regarding execution.

Execution of Directed Orders

The execution of directed orders involves multiple players, including exchanges, broker-dealers, and market makers. When we issue a directed order, it bypasses some of the broker’s regular order routing processes. We directly affect the market liquidity of the security in question, because the order is intended for a specific venue, which may offer different benefits such as improved execution prices or rebates. Directed orders are particularly relevant for limit orders, where we specify the maximum or minimum price at which we are willing to buy or sell a security.

Order routing, in the case of a directed order, is the conscious path we choose to potentially optimize for market conditions such as price improvement opportunities or to participate in different liquidity venues that may offer rebates.

Benefits and Risks of Directed Orders

There are both benefits and risks with directed orders.

- Benefits:

- Offers more control over the execution process.

- Potentially better execution prices due to targeting specific liquidity pools.

- Improved chances of order fills at desired prices, and sometimes participation in unique liquidity rebates offered by certain exchanges or market makers.

- Risks:

- May lead to narrower liquidity, as the order is restricted to a particular venue.

- Not always guaranteed the best execution, as market conditions may shift rapidly, and other venues may offer better prices.

- Increased complexity in order routing, which requires a solid understanding of exchange operations and fee structures.

As we analyze directed orders, it is essential to weigh these benefits against the potential risks. While we possess increased control over our order flow, we also take on the responsibility for the associated outcomes, which can include both the positive impacts of targeted liquidity and the negative consequences of missed opportunities in other parts of the market.

Broker-Dealer Dynamics

In the financial marketplace, broker-dealers play a pivotal role in the routing and execution of orders, balancing their responsibilities alongside potential conflicts of interest to maintain transparency.

Role of Broker-Dealers in Order Routing

Broker-dealers hold a significant responsibility in the process of order routing. They act as intermediaries between buyers and sellers and have the discretion to determine how and where to route clients’ orders. Rule 606, commonly referred to as the Order Routing Disclosure rule, requires brokerage firms to disclose information about the routing of non-directed orders to foster transparency. We find that ensuring best execution—filling customer’s orders at the most favorable terms possible—remains at the forefront of a broker’s duties. Broker-dealers may receive compensation or commission for directing orders to particular exchanges or market makers, an arrangement known as Payment for Order Flow (PFOF).

- Brokerage Firm: The entity that employs brokers to facilitate transactions.

- Brokers: Individuals tasked with the execution of trades on behalf of clients.

- Dealers: Entities that trade on their own account.

- Discretion: The choice brokers have in order routing.

Conflict of Interest and Transparency

Conflicts of interest within the brokerage industry can arise when a firm benefits from the order flow more than the client does, especially if the compensation structure for the broker-dealers influences the decision-making process. Complete disclosure of potential conflicts is mandated by regulators to ensure that clients can make informed decisions. We adhere to these transparency guidelines, as evidenced by detailed quarterly reports required under Rule 11ac1-6, now known as Rule 606. These reports give comprehensive insight into the handling of orders, revealing whether a broker-dealer has an economic incentive that could potentially conflict with the best interests of its clients.

- Conflicts of Interest: Situations where broker-dealers’ benefits may not align with client interests.

- Transparency: The clarity and openness with which brokers must operate regarding order routing and financial incentives.

- Disclosure: Providing necessary information to clients about how orders are routed and potential conflicts of interest.

Technological Impact on Directed Orders

In the realm of financial markets, technology has dramatically transformed the way directed orders are handled, emphasizing speed, efficiency, and sophistication through algorithmic trading and ECNs.

Algorithmic Trading and Order Execution

We have witnessed a substantial shift in trade execution as algorithms have begun to dominate the process. Algorithmic trading utilizes complex formulas and high-speed computations to follow a set of instructions for placing trades in order to generate profits at a speed and frequency that is impossible for a human trader. The crux of this advancement lies in algorithms and quantitative-driven investment strategies, which seek out arbitrage opportunities and execute trades within milliseconds. These algorithms are ingrained with machine learning capabilities, which enable them to adapt and improve their decisions based on market data trends.

This approach has not only changed how orders are directed but also the very fabric of market operations, making it crucial for investors to understand the nuances of these systems. For instance, our own directed orders are now capable of scanning multiple markets simultaneously to find the best venue for execution, taking into account factors like price, liquidity, and timing.

Electronic Communication Networks and Liquidity

Electronic Communication Networks (ECNs) have been key in providing a platform for direct trading among market participants, effectively bypassing traditional market intermediaries. ECNs offer enhanced market liquidity by connecting various buyers and sellers who wish to trade directly.

As we engage with ECNs, we find that they offer transparency, lower costs, and after-hours trading, which are significant benefits for our market strategies. The real-time order book provided by ECNs allows us to assess market liquidity instantly and make informed decisions about where to route our trades for the best possible execution.

Comparing Directed and Non-Directed Orders

When we trade in the financial markets, we often choose between placing directed and non-directed orders, which are distinct approaches to the execution of stock trades. Understanding these differences is crucial for us to optimize our trading strategy, whether we’re an active trader or a retail investor.

Key Differences Between Order Types

Directed Order Flow: A directed order is an instruction we send to a broker specifying the venue where our trade should be executed. This is often used by active traders who have a preference for a particular exchange due to pricing advantages or the speed of execution.

Non-Directed Orders: In contrast, non-directed orders are handed over to a broker without specific instructions on where to route them. Brokers have the autonomy to select the execution venue that may provide the best execution in terms of speed, price, and likelihood of execution.

- Pricing: With directed orders, we can aim for pricing improvements such as price breaks or a penny per share rebate. This can make a significant difference, especially for large volume trades.

- Order types: Directed orders can be both passive or aggressive. Passive orders do not immediately consume existing liquidity in the market; they add to the market’s depth. Aggressive orders, conversely, match against existing orders on the books, consuming liquidity.

It’s important for us to recognize the ramifications of each order type on our trading strategy. By leveraging directed orders effectively, we could potentially increase our returns or decrease transaction costs. Non-directed orders, while relinquishing some control over execution, provide the convenience of not having to select a specific venue.